Should You Dollar Hedge Your Foreign Bonds?

A well-diversified investment portfolio should at least include bonds as well as stocks. And in the case of bonds, you will discover that there are more sub-asset classes than there are for stocks. Today I’m focusing on bonds issued by foreign governments. One of the challenges with those kinds of bonds is that as a retail investor it can be difficult (and expensive) to buy them. In addition, there’s a risk associated with bonds denominated in foreign currencies that you don’t face when investing in U.S. bonds, namely currency risk. If the currency of the country from which you purchased the bonds drops in value relative to the U.S. dollar, any return from the bonds will be reduced by the same degree as the currency devaluation. (The opposite is also true when the local currency exchange rate improves). Fortunately, there are ways around both these challenges. There are numerous mutual funds and ETFs available in the U.S. that invest in foreign bonds quite efficiently, making it easy to add some to your portfolio. And some of them utilize what is called dollar hedging to eliminate currency risk, while others do not. Is it better to invest in a dollar-hedged foreign bond fund or to stick with those whose returns additionally fluctuate based on currency exchange rates?

Let’s start with a brief explanation of the way dollar hedging works. As an example, we’ll look at Japanese sovereign bonds and will pretend that the current exchange rate is one hundred yen to the dollar. Suppose a mutual fund wants to buy a ¥100,000 Japanese government bond maturing in one year with a coupon rate of 10%. The most common way to hedge against currency risk is to purchase both the bond (using $1,000 converted to yen) together with a forward contract agreeing to sell ¥110,000 for U.S. dollars one year from now at today’s exchange rate. When the fund sells the bond the following year, it also simultaneously closes out the forward contract. Those two actions effectively eliminate any currency impact on the expected return of the bond. The purchaser will get a 10% return on their investment in dollars, less the cost of having purchased the forward contract.

If foreign bonds can be boosted as well as reduced based on currency exchange rate changes, why bother to hedge against them at all? Why not just live with the losses or enjoy the extra gains from any currency movements? The primary reason is because currency fluctuations are much more volatile than bond price fluctuations.

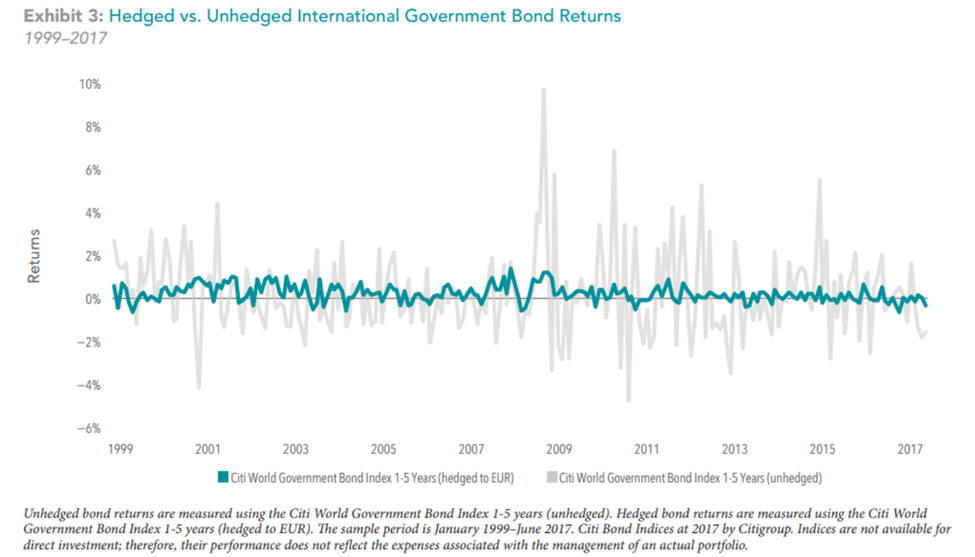

See the chart below put together by Sam Instone at AES wealth. The light gray line shows the returns from an unhedged international government bond index over a recent twenty-year period in Euros (for a European investor). The blue line shows the same returns over the same period but using an index hedged against the Euro. Note that although the average annual return of both indices is almost the same (2.9% versus 3.0%), the hedged index has significantly lower volatility (1.3%) as compared to the unhedged index (6.5%).

You can see how the volatility introduced by currency fluctuations swamps the volatility from the bonds. A mutual fund or ETF based on this index would be acting more like a foreign currency fund than a foreign bond fund. It would also fail to provide the level of portfolio stability that bonds are expected to do.

You might also ask if you should hedge investments in foreign stocks as well. It’s not necessary because with stocks, equity volatility is generally higher than currency volatility. Since dollar hedging does add additional cost to a fund, there’s not much benefit to applying it to equities.

If you are going to include international bonds in your portfolio, a fund that hedges out currency risk is more likely to provide the diversification and stability you’re looking for than one that doesn’t.

(Artie Green is founder of Cognizant Wealth Advisors dba Perigon Wealth Management, LLC, a registered investment advisor. For more information visit cognizantwealth.com. More information about the firm can also be found in its Form ADV Part 2, which is available upon request by calling 877-977-2555 or by emailing compliance@perigonwealth.com).